The Transfer Balance Cap (TBC) limits how much superannuation you can transfer into tax-free retirement phase pensions over your lifetime. Your personal TBC is individually tracked by the ATO through your Transfer Balance Account (TBA) and is based on your highest ever retirement-phase balance, not your current balance.

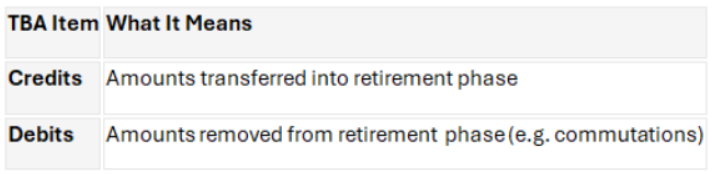

How the Transfer Balance Account (TBA) Works

The TBA is a lifetime record of movements into and out of the retirement phase.

Investment earnings, pension payments, and market movements do NOT affect your TBA.

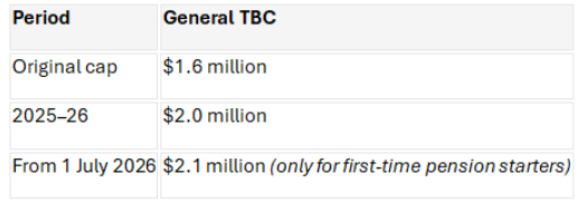

General Transfer Balance Cap Levels

How Your Personal TBC Is Determined

1. First-Time Pension Starters

Your personal TBC equals the general cap in force when your first pension begins.

- 2025–26 starters: $2.0 million

- From 2026–27 starters: $2.1 million

2. Existing Pension Holders

If you started a pension earlier, your cap:

- Is not reset to the new general cap

- Is based on your highest ever retirement balance

- Increases only via proportional indexation

3. Proportional Indexation

When the general cap increases, you only benefit if you had unused cap space.

Example: If you had used 60% of your cap, you receive 40% of any future increase.

What Creates TBC Credits and Debits?

TBC Credits

- Starting a retirement phase pension

- Certain structured settlement contributions

- Defined benefit income streams (special valuation applies)

TBC Debits

- Full or partial commutations

- Pension lump sum withdrawals

- Death benefit pensions being commuted

- Family law splits

- Fraud, bankruptcy, or non-complying pensions

Defined Benefit Pensions (Special Rule)

Lifetime defined benefit pensions are valued using a special value:

Annual pension × 16

- Based on the first annual entitlement

- Later pension increases usually do not create new TBC credits

- Can significantly use TBC space despite being non-commutable

Exceeding Your Transfer Balance Cap

Exceeding your personal TBC results in:

- Excess transfer balance tax

- Daily notional earnings

- Possible ATO enforcement action

How to Fix an Excess

- Commute the excess back to accumulation or withdraw it

- Act quickly to minimise tax

- Voluntary action is better than waiting for the ATO

- Death benefit pension excesses must be withdrawn as a lump sum

What Does Not Affect Your TBC

Your TBC is not recalculated for:

- Investment growth or losses

- Pension payments

Only formal credits and debits change your balance.

Understanding your personal Transfer Balance Cap is essential to:

- Maximise tax-free retirement income

- Avoid excess transfer balance tax

- Make informed pension and commutation decisions

Because indexation is proportional and permanent, early planning and professional advice can significantly improve outcomes.

For More Information visit our Website

Reach out to us at biz@carisma-solutions.com.au

Connect with us on our WhatsApp.

Credits

Sundaram Shanmugam, Smart SMSF Team