Thinly Capitalised Entity

- A thinly capitalised entity is one whose assets are funded by a high level of debt and relatively little equity.

- Such an entity is said to be highly geared.

- An entity’s debt–to–equity funding is sometimes expressed as a ratio.

Problems of High Gearing

- A high gearing ratio creates problems for:

a) Creditors – Who bear the solvency risk of the entity

b) Tax Authorities – Who are concerned about the excessive interest claims

Credit Risk

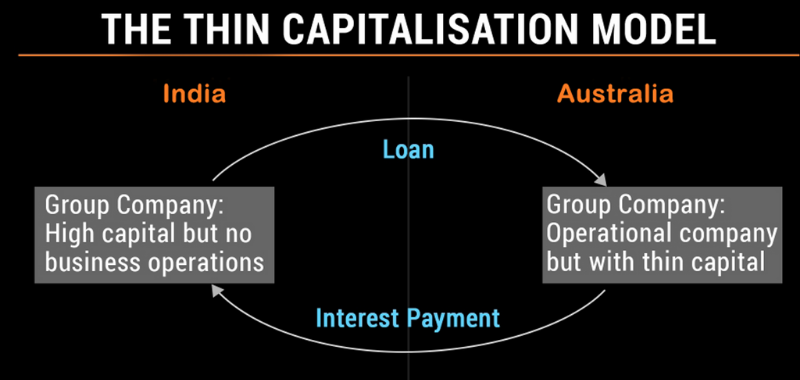

- In most cases, the company’s capital comes from debt funds when the promoters have introduced only nominal capital.

- Ultimately these debt funds are to be serviced by paying interest on a periodical basis.

- This indicates that the providers of these debt funds are directly competing with the company’s trade creditors for the same resources.

Thin Capitalisation Rules

- Under the thin capitalisation rules, the amount of debt used to fund the Australian operations of foreign entities investing in Australia and Australian entities investing overseas is limited. The rules disallow a deduction for a portion of specified expenses an entity incurs in relation to its debt finance; that is, its debt deductions. The rules apply when the entity’s debt-to-equity ratio exceeds certain limits.

Applicability

- Australian entities with specified overseas investments – these entities are called outward investing entities

- Foreign entities with certain investments in Australia – these entities are called inward investing entities

Non – Applicability

- You are an Australian resident entity that is not an inward investing entity nor an outward investing entity.

- You are a foreign entity that has no investments (such as assets) or permanent establishment in Australia.

- You meet any of the three threshold tests

a) Your debt deductions, together with those of any associate entities, are $2 million or less for the income year.

b) You are an outward investing entity that is not also foreign-controlled, and you meet the assets threshold test.

c) You are a special purpose entity established to manage certain risks.

Who Is Affected?

Types of Entities

The thin capitalisation rules apply differently depending on whether an entity is:

- An Authorised Deposit Taking Institution (ADI)

- A General Entity or a Financial Entity

- A Non – ADI General Entity.